Article

Asia as a source of diversification for global investors

24 March 2023

Diversification was hard to come by for global investors last year. Rising U.S. interest rates sank almost all boats in a coordinated sell-off across capital markets: U.S. equities were down 18.1%, U.S. investment-grade bonds were down 15.6%, nominal Treasuries were down 12.5% and inflation-linked Treasuries were down 11.8%. European assets followed a similar path, with deviations linked primarily to the differential between local rates and U.S. rates (and the resultant impact on currencies).

The story in Asian markets was quite different.

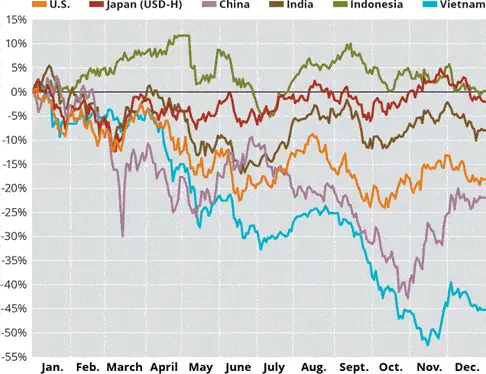

In China, domestic policy decisions on COVID-19 restrictions, real estate developer leverage and technology company regulations had a significant impact on market returns. Chinese equities finished the year down 21.8%, slightly worse than the U.S. but following a very different path. Chinese equity markets were up 3.2% in the second quarter of 2022 when the U.S. was experiencing its largest quarterly loss for the year (-16.1%).

Chinese monetary policy took a stimulative stance taking rates down from 3.8% to 3.65% to address the various headwinds facing the economy, which resulted in China being the rare market to experience positive returns for government bonds.

In India, the economy needed no monetary stimulation, with domestic development tailwinds outweighing global headwinds to make India one of the fastest growing large economies. Despite India seeing record net outflows of $16 billion from foreign investors through the year (equivalent to -0.5% of the aggregate market cap), domestic sentiment on equities remained strong and the equity market was up 3.0% in Indian rupee terms (though down 8.0% in U.S. dollar).

Japan held firm to their yield curve control approach through most of the year, maintaining relatively flat equity market performance while seeing the yen drift as low as ¥150/$ vs. ¥115/$ at the start of 2022. In the smaller markets of Southeast Asia, there were also significant deviations in performance, with Indonesia and Thailand generating positive returns (in local currency and U.S. dollar terms), while Vietnamese equities lost more than 40% of their value. The spread of performance of these various markets is shown below.

It is clear from the broad range of market outcomes through the year that Asia is moving to its own beat. This is a trend that has continued in 2023, with the key issues of bank balance sheet risk being less of a concern in Asia given banks in the region had a significant wake-up call in the Asian financial crisis and they currently have a more attractive set of lending opportunities to deploy deposits in to given the stronger corporate growth rates.

The region is not immune to the challenges faced by Western countries of inflation and rising rates, but most Asian countries were not affected by the uncharacteristically low inflation and interest rates in the preceding decade. Their economies, policies and decision-making frameworks have more experience dealing with uncertainty and volatility.

The Asia-Pacific region is increasingly driven by domestic consumption and intra-regional trade (59% of Asia trade was intra-regional in 2020, a three-decade high). That all contributes to the reliance and increasingly idiosyncratic returns we see coming from the region.

With independence, there is a greater degree of uncertainty, however, and Asia does face its own challenges ahead in the form of political and economic restructuring. To fully utilize these diversification benefits requires significant understanding of key return drivers within the region.

How much should be invested in Asia-Pacific assets?

Investor allocations to Asia-Pacific vary significantly depending on how well positioned the investor is to assess the key return drivers across the region. Allocators within Asia often have more than half of their portfolio invested in the region, while those outside the region may have no allocation at all.

| Country/region | Bond makeup (WGBI) | Equity makeup (ACWI) | Total makeup |

| Japan | 14.9% | 5.4% | 9.2% |

| China & Hong Kong | 2.1% | 4.1% | 3.3% |

| Australia & New Zealand | 1.3% | 2.0% | 1.8% |

| Taiwan | — | 1.7% | 1.0% |

| India | — | 1.5% | 0.9% |

| South Korea | — | 1.3% | 0.8% |

| ASEAN | 0.7% | 1.0% | 0.9% |

| Total | 19.1% | 17.0% | 17.9% |

A standard global 60/40 equity/bond benchmark (MSCI All Country World index/FTSE World Government Bond index) has an allocation of 18% exposure to Asia-Pacific (or 16% excluding Australia and New Zealand). While Asia represents less than 50% of global gross domestic product, a 15-20% portfolio allocation would seem appropriate for a diversified global investor. Beyond the aggregate weighting guidance, this approach to benchmarking provides little sensible insight on how allocations within Asia should be split. For example, two-thirds of the total exposure in the benchmark comes from Japanese government bonds that have expected returns of 0.5% if held to maturity and face significant mark-to-market risk if rates increase.

When it comes to setting country allocations, we encourage investors to embrace the markets in Asia that present the deepest opportunity set for capital deployment and the greatest diversification benefits.

India and China are first and foremost here. Combined, the two represent a population of approximately 3 billion people, who are experiencing rapid growth in their incomes with a significant runway to catch-up to their developed counterparts.

India and China differ significantly across stages of development, political structures, demographics, industry focus and competitive advantages — all of which have contributed to historically low correlation to both developed markets and to each other.

The next largest economies in developing Asia are South Korea and Taiwan, but for global investors these are relatively less interesting. Their successful growth model of developing globally competitive national champions in the electronics industry has left the opportunity for capital deployment more narrow and more correlated to global consumption. Japan has some of the characteristics of South Korea and Taiwan, but is a larger and more diversified economy so it presents more interesting opportunities, particularly on a thematic basis (e.g., corporate governance reform and the switch from analog technologies to digital).

Southeast Asia is expected to grow at 5-6% over the coming years, creating attractive opportunities for directional and dispersion-based investments, but execution at scale within a portfolio remains challenging due to the lower liquidity and trading volumes in the region.

Executing an Asia strategy in 2023

Historically, there has been a misplaced belief that higher economic growth in Asia will result in higher equity market returns— leading investors to focus almost solely on the equities asset class.

The reality is that higher growth benefits only a small subset of high-performing businesses, while leading to a greater number of companies being created and higher volatility/dislocations within markets.

These characteristics point more clearly to opportunities emerging in the alternatives space (e.g., hedge fund and private equity). The alternatives space in Asia has seen several tailwinds over the last 10 years, specifically an increase in the availability of cost-effective instruments for trading (e.g., derivatives); an influx of investment talent returning from best-in-class global funds, who then trained the next generation of local portfolio managers; and a rich opportunity set in markets that are still primarily dominated by retail investors.

Alternative strategies that we are particularly excited about in the current environment are Asia long-short credit, Asia macro, Japanese equity market neutral, Indian venture capital, and Southeast Asian private debt. In the near term, many of these market niches remain capacity constrained, so building long-term relationships on the ground with high-quality independent asset managers is important.

Asia is a region often poorly understood and underappreciated by global investors. Long-term growth potential, near-term dislocations in valuation and portfolio construction benefits all favor taking a closer look and understanding what role a diversified portfolio of Asian opportunities can play within a global investment portfolio.

This was originally published on 24 March 2023 in Pensions & Investments.