Article

Inflections: SpaceX and the 2026 IPO Wave – What It Means for the Broader Market

2 July 2026

In 1964, Soviet scientist Nikolai Kardashev proposed measuring a civilization’s level of advancement based purely on the amount of energy it could harness: a Type I civilization commands all energy on Earth; a Type II, all the energy of the Sun; and a Type III, all the energy of its galaxy. By Kardashev’s standard, we remain a Type 0, and scientists such as Dr. Michio Kaku estimate that graduating to a Type I status is still 100 to 200 years away.

However, Elon Musk does not want to wait that long.

Enter SpaceX

Musk has explicitly cited the goal of advancement on the Kardashev Scale as a justification for SpaceX when laying out the design of SpaceX’s AI1 satellite. AI1 will be the first generation of orbital craft SpaceX wants to build by the millions to run AI workloads using solar energy in Space, away from Earth’s power grid. If successful, he will have addressed many of the existing data center issues on Earth, from energy provision to real estate and environmental limitations. Using Starlink to beam tokens back and forth also bypasses fiber networks that may be vulnerable to disruption. In the best-case scenario, it could at least partially displace the trillions of dollars of investment going into terrestrial data centers.

There are, however, significant challenges. SpaceX’s S-1 IPO filing warns the company currently cannot secure enough chips, which is partly why it is building Terafab, a chip fab run as a joint venture with Tesla and xAI. As a further hedge, the AI1 spacecraft uses an interchangeable hardware design that lets different chipmakers supply the processors.

Another major constraint is cooling. Musk pegged the satellite’s compute payload at roughly the draw of a single Nvidia GB300 rack, which pulls around 140 kW on the ground. A rack on Earth sheds heat into moving air and circulating water, neither of which exists in a vacuum, where the only viable discharge route is radiating it away as infrared.

Unsurprisingly, there is a broad spectrum of views on whether the above opportunity set justifies the price. The IPO came in at a $1.75T initial market valuation ($135/share) and the stock now is valued c. $2.2T ($170/share). Morningstar has modeled a range of scenarios, assuming in all cases that by 2035 SpaceX will be able to launch 340 Starship missions a year, nearly one a day. However, only its most optimistic scenario puts SpaceX’s fair value near the IPO launch valuation. In fact, their probability-weighted valuation across all scenarios is significantly lower, at only $63/share.

Yet, Musk has frequently confounded skeptics in the past. Few would have thought he would surpass both Boeing and Lockheed Martin in successful space launches, particularly with reusable rockets. In addition, the ‘Musk’ brand is worth a great deal. If Tesla is any indicator, SpaceX can run higher as investors (and passive funds) build positions. Over the longer term, the stock will likely converge to its fundamentals.

Looking beyond SpaceX

Regardless of how SpaceX ultimately performs, it is one name in a larger wave of new entrants and the more consequential question for investors is not what any single listing is worth, but how a flood of new supply can impact the overall market.

- After several years of muted flows, the next few months appear primed to bring a significant uptick in IPO activity that will challenge previous 2021 and 2000 peaks.

- The upcoming IPO pipeline likely includes companies currently valued at more than $4T, equivalent to 6% of current S&P 500 market cap, inclusive of SpaceX at its original IPO valuation of $1.75T.

- This could represent over $200B of incremental US equity market capitalization to be absorbed (assuming an initial weighted average float of approximately 6%).

- Three companies account for more than two-thirds of that on their own: SpaceX1 IPO’d at $1.75T (now higher), Anthropic2 is valued at $0.97T, and OpenA3 is valued at $0.87T.

What happens after large IPO waves?

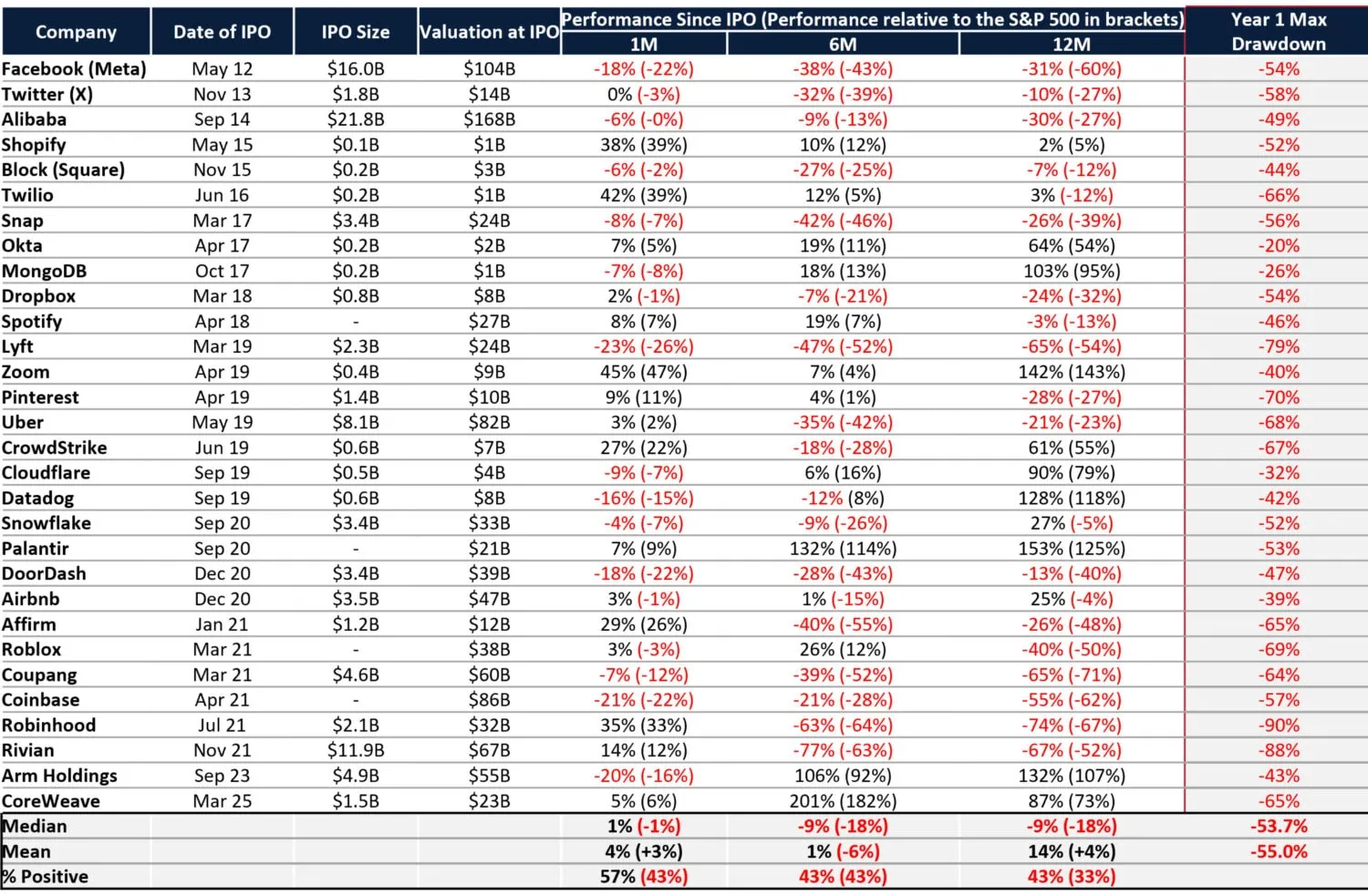

While IPOs typically experience a jump in valuation in the early days following listing (almost by design), a somewhat longer-term review of performance reveals less attractive outcomes. In Table 1 below, we ran the numbers on 30 of the largest tech listings (both IPO and direct) over the last 15 years.

Notably, all 30 firms experienced a significant drawdown at some point in their first year of trading, even if they subsequently recovered.

In order to exclude the effect of broader market movements, the figures in brackets show performance relative to the S&P 500.

Table 1: Large tech listings typically experience significant drawdowns in the first year

(Brackets indicate performance relative to the S&P 500)

Source: Bloomberg, Partners Capital Analysis

The past may not represent the future and, even in the above dataset, some companies fared well. The difference between the median and mean outcomes suggests there is a wider right tail to the big winners.

IPOs’ footprints on broader market performance

A recent study by BCA4 focused on 12,000 IPOs over 40 years, suggests that although heavy IPO supply does not necessarily preclude a bear market, it can dampen equity market performance, mute multiple expansion and possibly interrupt sector trends.

For example, in the 12 months following an IPO from the largest quintile, the median S&P 500 index return was -4% below the unconditional median, with an interquartile range that indicated a significant probability of negative returns. Roughly speaking, forward 12-month returns are negative about 20% of the time following top-quintile IPOs.

But this analysis does not suggest that large IPOs necessarily lead to significant market downturns. Some large IPOs have coincided with local market peaks, such as Goldman Sachs in 1999, Palm Inc. in 2000, Blackstone in 2007 and Glencore in 2011, which marked a major peak in commodities. However, many large IPOs occurred amid extended bull markets, such as Twitter (2013) and Spotify (2018). Similarly, market drawdowns, even significant ones, do not always coincide with sizeable IPOs. The relationship is not deterministic.

Overall, the study suggests the current IPO wave may pose more of a headwind to forward returns and multiple expansion than a catalyst for a sustained bear market. The greater risk is not whether the market can absorb the supply, but whether investors are likely to fund new AI and tech issuance by trimming the existing winners that, until now, have been the scarce way to own the theme. The danger is then less a market that cannot digest the new supply, but a leadership that quietly rotates beneath it.

As noted in Partners Capital Insights 2026, we have focused our AI/tech investments less on the hyperscalers in the Mag-7, and more on the ‘picks and shovels’ of infrastructure providers through our expert specialist managers in both public and private markets. Our venture investments have held exposure to many of the leading names in the IPO funnel. However, we are also monitoring potential inflection points in capex spending and the implications for the downstream beneficiaries.

For now, investors will be more focused on navigating market volatility rather than advancing from a Type 0 to Type I Kardashev civilization.

Sources

- Bloomberg, SpaceX Has Filed Confidentially for IPO Ahead of AI Rivals (1 April 2026)

- Anthropic, Anthropic raises $65B in Series H funding at $965B post-money valuation (28 May 2026)

- Bloomberg, OpenAI Nears $100 Billion Funding at $850 Billion Valuation (19 February 2026)

- BCA Research, “Monster IPOs: Too Big to Float?” (8 June 2026)